## Understanding UAE Invoice Requirements: Beyond Just a Total

Navigating the intricacies of invoice requirements in the UAE goes far beyond simply stating a total amount due. While the final figure is undeniably important, the Federal Tax Authority (FTA) mandates a comprehensive set of details to ensure transparency, compliance, and accurate tax reporting. Businesses, especially those dealing with VAT, must understand that a compliant invoice isn't just a receipt; it's a critical legal document. Failure to include essential elements can lead to significant penalties, delayed payments, and even disputes with customers or suppliers. Therefore, a thorough understanding of these requirements is paramount for maintaining good standing with the tax authorities and fostering efficient business operations within the Emirates.

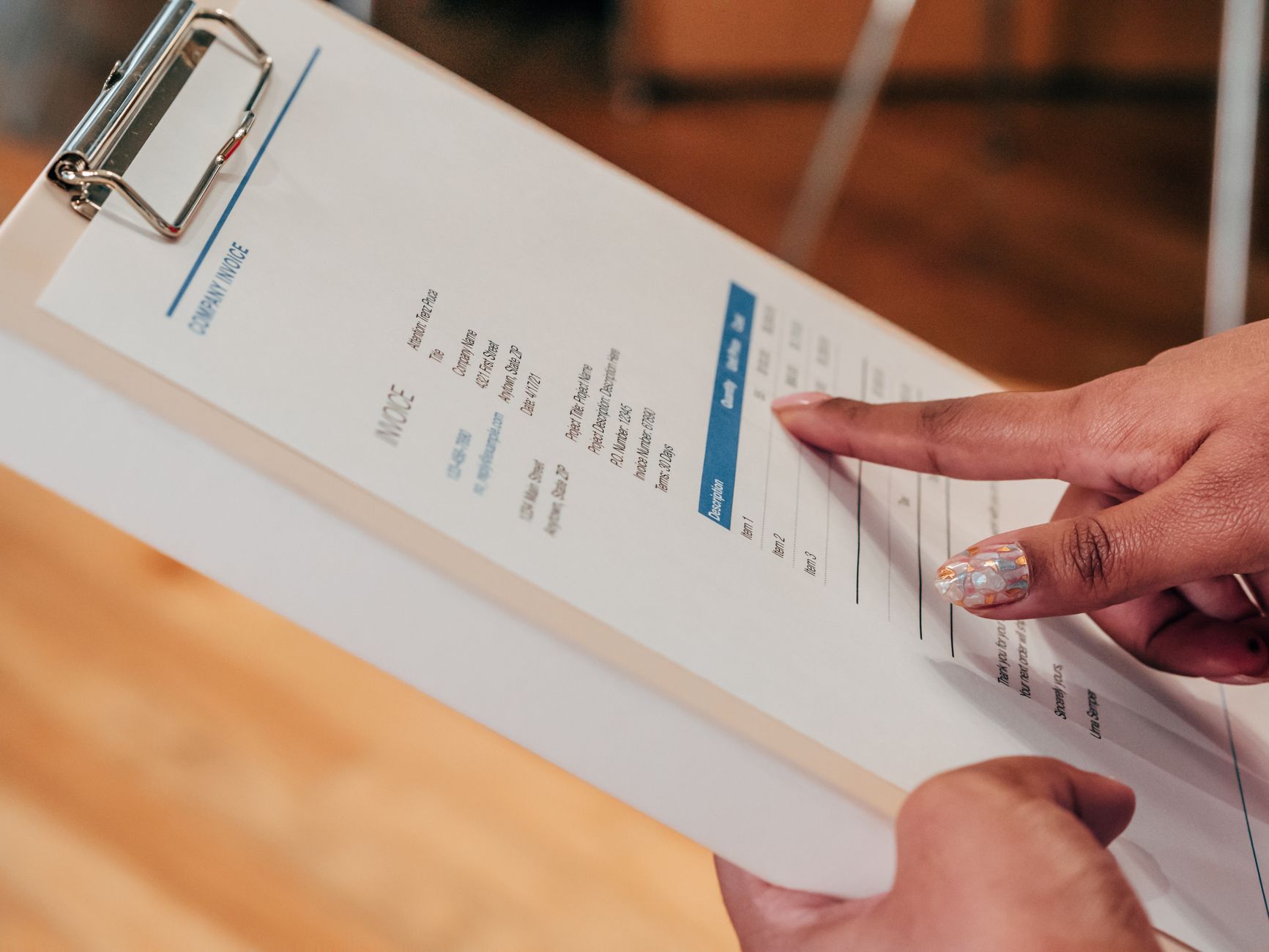

A properly structured UAE invoice serves as the bedrock for accurate record-keeping and robust financial management. Key elements that often extend beyond just the total include:

- Supplier and Recipient Details: Full legal names, addresses, and TRNs (Tax Registration Numbers) are mandatory.

- Unique Invoice Number & Date: Each invoice must have a distinct identifier and clear date of issue.

- Description of Goods/Services: Detailed and unambiguous descriptions are crucial for tax classification.

- Unit Price & Quantity: Transparent breakdown of costs before any taxes.

- VAT Amount & Rate: Clearly stated VAT percentage and the corresponding amount, if applicable.

- Total Amount Payable: This includes the net amount plus any applicable taxes.

Adhering to these specifications not only ensures compliance but also streamlines audits and reduces the likelihood of discrepancies.

To issue an invoice, start by gathering all necessary details like your company's information, the client's information, a unique invoice number, date of issue, and a clear breakdown of services or products provided with corresponding costs. Make sure to include any applicable taxes, the total amount due, payment terms, and your preferred payment methods. For more information on how to issue an invoice, ensure all details are accurate and the invoice is sent promptly to your client.

## Practicalities & Pitfalls: What Happens After You Issue an Invoice?

Once an invoice is issued, the ball is truly in motion, and the focus shifts to ensuring timely payment and maintaining clear communication. The initial period after sending an invoice often involves a period of watchful waiting, but it's also crucial for proactive monitoring. Savvy businesses will have a system in place to track the invoice's status, noting the payment due date and any agreed-upon terms. This might involve a simple spreadsheet for smaller operations or sophisticated accounting software for larger entities. Furthermore, anticipate potential queries from your client. Be prepared to provide additional details, clarify line items, or resend the invoice if it was misplaced. A prompt and professional response to these inquiries can significantly smooth the payment process and prevent unnecessary delays. Remember, your goal is to make it as easy as possible for your client to pay you.

Should the payment due date pass without remittance, a structured follow-up process becomes essential, but always approach it with professionalism and a problem-solving mindset rather than an accusatory one. Your first step might be a gentle reminder email, perhaps including a copy of the original invoice and highlighting the due date. If that doesn't yield results, a phone call can often be more effective, allowing for a direct conversation about any potential issues or misunderstandings. It's vital to document all communication regarding overdue invoices, including dates, times, and the content of discussions. This documentation is invaluable should further action be required.

While legal action is a last resort, having a clear paper trail of your efforts to collect payment strengthens your position.Ultimately, the aim is to recover the outstanding balance while preserving the client relationship where possible, as long-term partnerships are often more valuable than a single, difficult payment.